The year ahead promises to offer the housing industry some relief, compared with a grueling 2023, but it is likely to be only a small bounce forward toward a healthier market.

The housing industry, including the secondary market it feeds, is still likely to be sluggish in 2024, with marginal improvements in some sectors as others tread water or retreat slightly, industry players who spoke with HousingWire predict.

Still, a sluggish to slightly better forecast for 2024 beats the hardscrabble path of retrenchment the industry endured in 2023. Last year, fast-rising rates and related volatility, coupled with liquidity challenges in the bank and nonbank sectors, high home prices and a shortage of housing inventory all worked together to suppress mortgage originations and the secondary market outlets for those loans as well.

“Notwithstanding the recent mortgage rate rally [at yearend 2023], housing and mortgage markets will enter 2024 at approximately the same level as they entered 2023,” said Doug Duncan, senior vice president and chief economist at Fannie Mae, in the agency’s yearend commentary. “Thus, while we think home sales will start to rise over the new year, the combination of modest increases in home prices and still-elevated interest rates suggest a slow pace of recovery from previously recessionary levels of housing activity.”

John Toohig, head of whole-loan trading on the Raymond James whole-loan desk and president of Raymond James Mortgage Co., said many of the same headwinds the market faced in 2023 remain as we roll into 2024. He said among them are higher rates (down a bit at yearend, but still in the high 6% range); “… the lack of liquidity in the banking sector; increasingly challenged affordability; and [consumer] credit starting to show some early cracks on the lower end of credit and with younger borrowers.”

Still, an interest-rate drop and soft landing for the economy, if the latter is truly achieved, will break some of the ice in a chilled housing market.

“For 2024, should the Federal Reserve determine they have overcorrected and start to lower rates [as indicated at the Fed’s December Federal Open Market Committee meeting], you will see a surge in trading volumes,” he added. “Discounts will be less impactful, loans will trade closer to par or gains again, and much of the frozen underwater coupons will transact again.

“Should credit break and the consumer buckle, [however,] you could see home prices fall, delinquencies and charge-offs on the rise and that will negatively impact pricing in a market with limited liquidity.”

It remains a guestimate game as far as when the Federal Reserve — which paused rates at its final meeting in 2023 — will decide to begin rolling back its benchmark rate in the year ahead from the current range of 5.25%-5.5%.

As 2023 moved toward a close, 30-year fixed rates had dropped into the mid-to-high 6% range. Few, if any, industry groups or market experts, however, have been accurate in predicting rates very far out in the current topsy-turvy market.

“If you look at futures, you’re looking at lower [Fed] rates by May of next year,” said Tom Piercy, chief growth officer at Incenter Capital Advisors (previously Incenter Mortgage Advisors). “I wouldn’t make a bet on it is because there’s just so much complexity in this.”

MSR sector

Piercy, whose shops advises both banks and nonbanks on mortgage servicing rights (MSRs) transactions, said the year ahead for MSRs will be impacted negatively if rates decline, but he adds rates would have to adjust downward significantly to accelerate loan-prepayment speeds, which would draw down the value of MSR packages. He said marginally lower rates would affect the returns holders of MSRs get from parked escrow accounts, however, which does impact MSR pricing.

Piercy expects that the combined MSR trading volume in the coming two years (2024 and 2025) will be on par with or slightly better than the combined trading volume of 2022 and 2023, when rates spiked and more than $1 trillion in MSR deals transacted each year.

“Over the next three years, including 2023, [we estimate] sub-$4 trillion [in MSR trades], maybe in the high $3 trillion [range], and again that’s for 2023 through 2025,” Piercy said. For 2023, slightly greater than 1.1 trillion in MSRs are expected to have traded, he added.

Part of that trading volume in 2024, Piercy said, is expected to be driven by MSR sales resulting from the continuing merger and acquisition (M&A) activity in the nonbank sector of the market.

“Unless there’s some type of pickup in the forecast for originations, I think you’re going to see still an active M&A market through 2024,” he explained. “Many shops will probably look to become part of a larger, more financially stable platform.

“We’re forecasting right now a fairly strong Q1 for MSR sales. I think it’s going to be a robust market.”

MBS sector

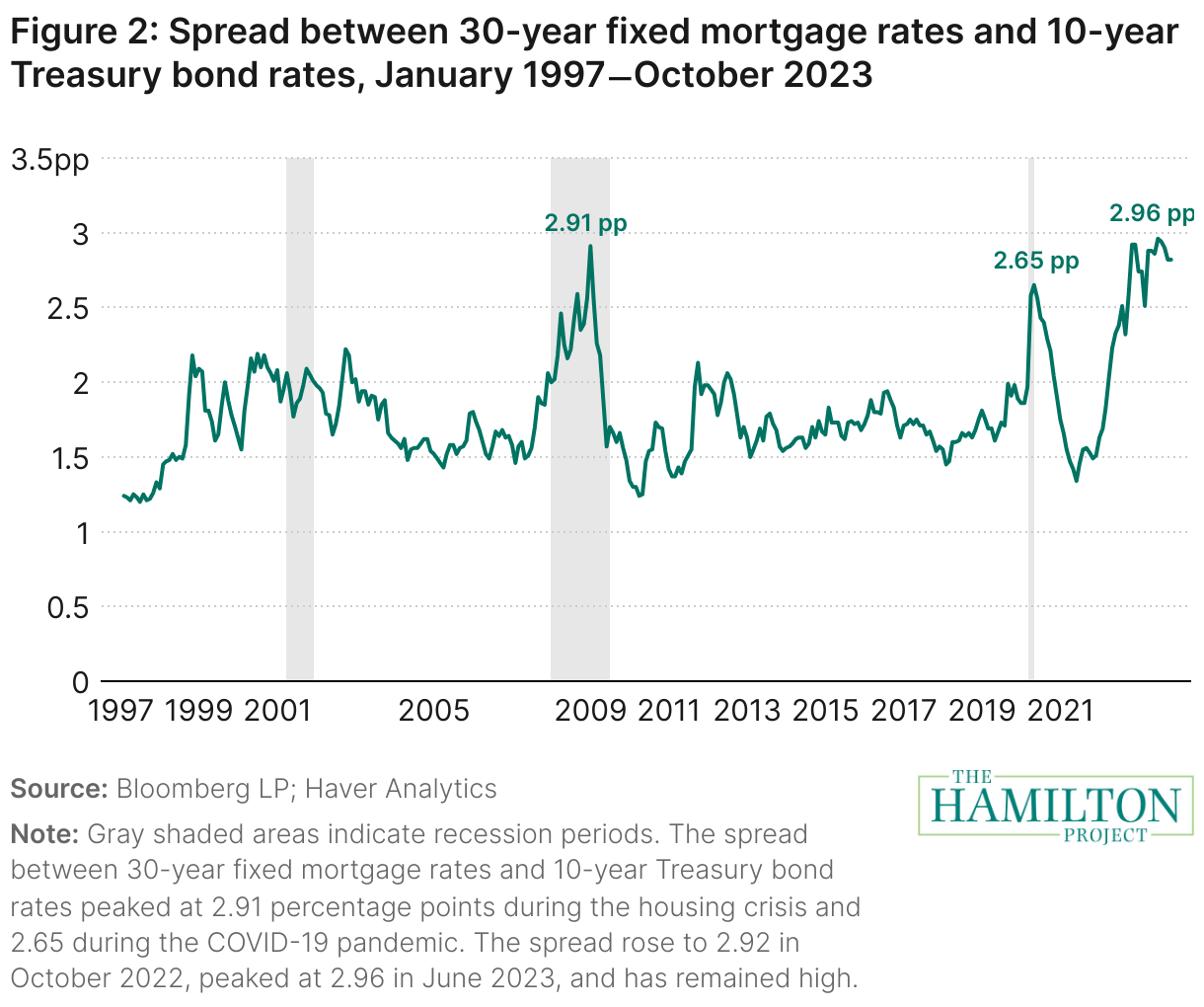

Robust is not the adjective to describe what’s ahead in 2024 for the agency (Fannie Mae, Freddie Mac and Ginnie Mae) mortgage-backed securities (MBS) market, however. Market observers say outsized spreads between the 30-year fixed mortgage rate and 10-year Treasuries and subpar MBS clearing rates are likely to continue, given the imbalance in supply and demand in the market as the Federal Reserve continues to unwind its $2.5 trillion portfolio of MBS.

According to projections by real estate investment firm the Amherst Group, agency MBS net issuance for 2024 is estimated at $300 billion, up slightly from $250 billion in 2023 — but still down significantly from the barnburner year in 2021, when net issuance totaled $870 billion. Net issuance in MBS represents new securities issued less the decline in outstanding securities due to principal paydowns or prepayments.

The Federal Reserve’s ongoing quantitative easing is expected to contribute an excess MBS supply to the market in 2024 of some $225 billion, which will need to be absorbed in addition to the projected $300 billion in net new issuance.

“Generally, our view has been that mortgages are really undervalued,” said Amherst Chairman and CEO Sean Dobson. “I’ve been doing this for 30 years, and they’re about as good in value as they’ve ever been.

“But we don’t see a lot of snapback, with mortgages getting back in line [in terms of interest rates] anytime soon. … Mortgage rates are high and one big reason … is the [agency MBS] investor base is impaired, and it’s not likely to be fixed soon.”

Dobson added that, in his view, monetary policymakers didn’t fully grasp that when the Fed stopped buying mortgages, “they had displaced the actual buyers for so long that the actual buyers are now gone.

“… Now you can buy billions of dollars in bonds [MBS] that are really undervalued relative to their intrinsic risk because there’s just no sponsor [a major new buyer since the Fed’s pullback].”

Richard Koss, chief research officer at mortgage-data analytics firm Recursion, also offers a bleak assessment of the agency MBS market ahead — primarily because mortgage originations are likely to remain depressed, which means agency MBS issuance will be depressed as well.

Koss points to the huge volume of low-rate mortgages outstanding as the vexing problem the market faces, adding that low-rate legacy (2020 and 2021) mortgage-backed pools “are mostly discount bonds in the current [high] rate environment.”

“All the 4.0% and lower mortgages that dominate the market are less than four years old,” he said. “If you have a 3% mortgage, you need a 2.5% rate to justify refinancing, which is a 1% Treasury yield.

“That could happen, but we don’t want it to, since it means some kind of disaster. I think a mortgage winter has frozen things hard and conditions are such that we can only expect a measurable improvement out past 2030.”

The Mortgage Bankers Association (MBA) estimates that total mortgage originations in 2023 will come in at about $1.6 trillion, down considerably from the $4.4 trillion in originations chalked up in the banner year of 2021. Next year, the MBA forecasts total originations at slightly more than $2 trillion — and its most current origination forecast shows only modest improvement in 2025, with originations (purchase and refinance) reaching $2.43 trillion.

RMBS sector

The origination downturn and rate volatility in 2023 negatively impacted the private-label residential mortgage-backed securitization (RMBS) market. Many market experts, however, expect a tailwind of declining rates for the year ahead as a result of recent signals from the Federal Reserve that rate cuts are on the table, starting as soon as the end of the first quarter of 2024.

“Additional rate hikes no longer appear to be part of the conversation, MBA senior vice president and chief economist Mike Fratantoni said in a statement reacting to the most recent Fed rate decision. “It is all about the pace of cuts from here.

“…We expect that this path for monetary policy should support further declines in mortgage rates, just in time for the spring housing market. We are forecasting modest growth in new and existing home sales in 2024, supporting growth in purchase originations, following an extraordinarily slow 2023.”

A report published in late November by Kroll Bond Rating Agency (KBRA) — which tracks RMBS offerings across the prime, nonprime, credit-risk transfer and second-lien sectors (RMBS 2.0). — assumed that the Fed was “closer to peak interest rates.” That assumption bodes well for the private-label market in 2024 — relative to its performance in 2023.

“We expect 2024 conditions to be more favorable and RMBS 2.0 issuance levels to be slightly higher than in 2023 at $56.5 billion (a 9% increase),” the KBRA report states.

Andrew Rhodes, senior director and head of trading at Mortgage Capital Trading, said the winter months ahead are going to be rough going for the housing market, including RMBS issuance.

“I think 2024 [overall] is going to be better from a [loan] origination standpoint, but I don’t think it’s going to be large increase,” he added. “…I really do think that 2025 will be a lot better, but that’s pretty far forward.”

Tailwinds

On a brighter note, Ben Hunsaker, portfolio manager focused on securitized credit for Beach Point Capital Management, points to the expansion of second-lien products in the primary market as a loan-origination and RMBS volume-driver in 2024, given the record-levels of home equity available to homeowners, many of whom are now locked into low-rate mortgages and have little incentive to sell or buy a new house.

“There’s this big pool of second liens and HELOCs [home equity lines of credit] that some of the originators have started to use as a key part of their toolkit, and you’re hearing them talk about it on earnings calls,” he said. “And so, I think that probably puts a kick in the pants to what 2024 [RMBS] volumes could look like.”

Charley Clark, a senior vice president and mortgage warehouse finance executive at EverBank (formerly known as TIAA Bank), also strikes a note of optimism for 2024 when it comes to the prospects for housing industry, specifically the large independent mortgage banks (IMBs) that feed the origination and securitization pipelines. Clark notes that EverBank serves about 40 of the largest mortgage banking companies in the nation.

“I think there’s definitely still some of the mom-and-pop shops [IMBs] — or let’s say a company with $20 million or $25 million or below in adjusted tangible net worth — that will be looking to sell,” he said. “But most of the big companies have solid balance sheets and have started to actually stop the bleeding.

“I’m encouraged because these companies [large IMBs] are much better positioned now. They’ve made the cuts, at least most of the cuts they need to make to right-size for where the industry is heading. And the best companies have really done a good job of that, so they’re positioned to do well next year, but it’s still going to be tough.”

Related

Source link

")

{kind=link}

{kind=link}